Happy Monday! If we may take ten minutes of your attention away from wrangling your Fable instance to build a prediction market trading bot with no mistakes — Ryan has produced a very enlightening essay on onion futures. If you ever wanted an awesome example of why you should hate the CFTC, this is it.

I’ve done some light editing, but otherwise this was entirely Ryan’s essay. If you want to check out his other work, here’s his author page on VoteHub, a PM-powered election forecasting company as well as an election decision desk.

Onions are terrible; they make me cry, and I have never once finished a meal wishing there were more of them. However, there is something that leaves an even worse taste in my mouth than onions: price instability, and even more so, the complete inability to hedge against it.

For any nerds reading this, you may remember this story from a Planet Money episode aptly named “The Tale Of The Onion King”. But I want to rehash it a bit. In 1955, two traders, an onion farmer named Vincent Kosuga and his produce-distributor partner Sam Siegel, cornered the Chicago onion market. They pushed the price to unseen highs and subsequently crashed it so violently that a fifty-pound bag, albeit briefly, sold for no more than the value of the bag itself.

Why manipulate the market just for the sake of creating volatility? How could you possibly benefit? His play was simple: accumulate a mountain of futures contracts while prices were still in the clouds, then reap the rewards once the market swung back in his favour. When Kosuga cornered the market and pushed prices to all-time highs, he sold a number of futures contracts, effectively locking in the high prices that he had artificially created. Then, to make his futures very, very valuable, he literally flooded the Chicago River with onions, which subsequently became plentiful and, for all intents and purposes, free. This caused immense pain for both farmers and speculators who had taken futures positions against him. Reactionary and absent-minded as usual, Congress banned onion futures outright in 1958. The law is still on the books, and onions remain untradeable on any futures exchange. The idea behind the ban was that banning those who wished to corner and manipulate the market would reduce the volatility of the onion market, therefore solving the flashpoint issue of the time: onion price volatility.

For just the briefest of moments, it is worth pausing on what exactly Congress banned, because a futures contract is not some exotic instrument (unless in the hands of a Robinhood day-trader). It is a promise to buy or sell at a set price on a set date, and for a farmer, it is closer to insurance than to gambling: lock in a price at planting (in fact, often before planting, to pay for implements) to protect yourself against a bad market during the harvest.

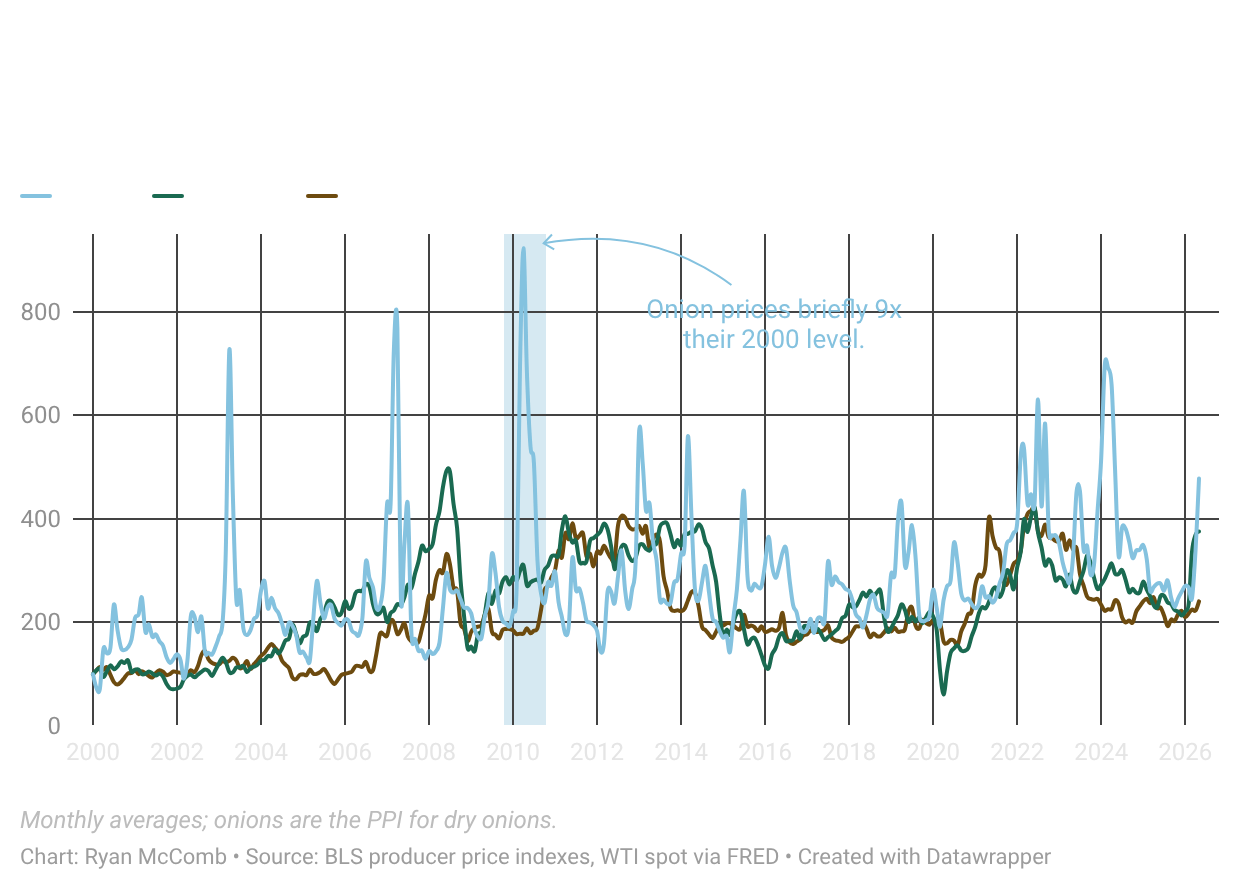

Futures markets also produce something subtler. It’s a rich source of very accurate public and private information in the aggregate, which creates a public forward price that everyone from growers to grocery chains can rely on. Onions have now gone 68 years without any of the benefits of these contracts, leaving a long and unusually clean, albeit cruel, natural experiment. Here is how it has gone, measured against crude oil and corn, two commodities known in and of themselves for being some of the most volatile on the boards of trade.

Even without consulting the legend, you can likely tell which line indicates onion prices. The spikes observed are not caused by a Datawrapper error (although it often glitches) — onion prices surged about 400 percent from October 2006 to April 2007, then plummeted 96 percent by the next March, and shortly afterward, tripled again. This pattern resulted from an unusually small onion harvest in 2006, combined with the fact that onion prices are highly inelastic (people buy roughly the same amount regardless of price changes). The subsequent March, prices fell sharply because farmers had accounted for the 2006 shortage and planted heavily in 2007. This happened, I will remind you, while cable news spent that same year blaming speculators for what oil was doing, and oil never managed anything half as undignified.

It really is truly impressive how volatile onions are once you strip away the futures contract. To manufacture swings like these in a Robinhood account, you would have to work hard: we are talking zero-DTE, OTM call options (the most dangerous financial derivative most retail traders can touch). The type of exposure people post to r/wallstreetbets right before deleting their life savings faster than they could give it away.1 Nevertheless, an onion farmer gets all of that by default, every season, without ever opening a brokerage account and seeing a gamified options chain on Robinhood. The difference is that the Robinhood trader chose this life.

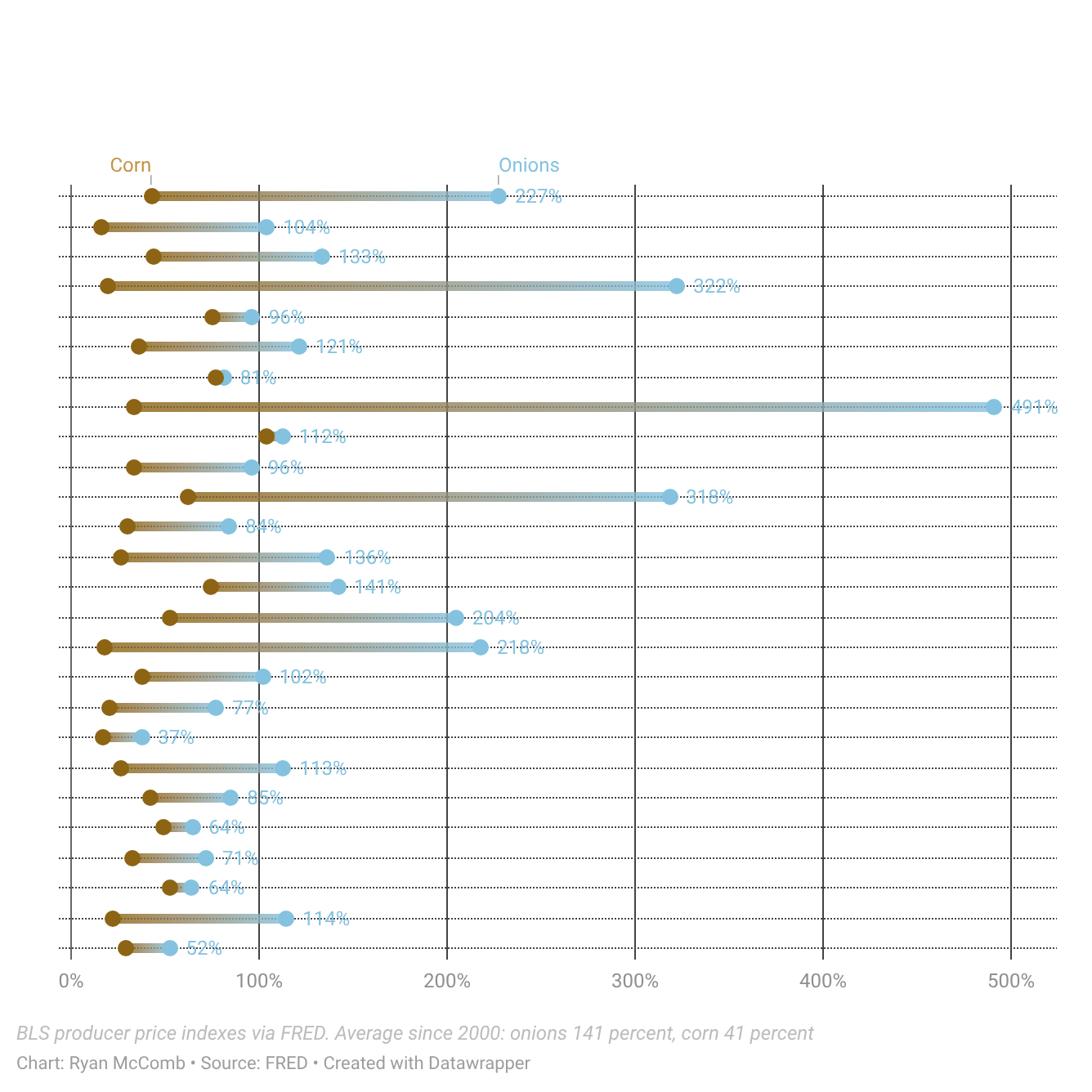

But one bad stretch does not make a case on its own. So sure, let’s take every year since 2000 on its own terms, and measure the gap between each year’s cheapest month and its most expensive, for onions and for corn, a hedgeable crop. Onions have not lost a single year.

The question of whether the ban worked is not a new one, and the first people to ask it did so with the ink barely dry. In 1963, the Stanford agricultural economist Roger Gray compared onion price behaviour across three eras: the decades before a futures market existed, the years the contract actively traded, and the years after Congress shut it down. His finding, published under the politely devastating title “Onions Revisited,” was that the onion prices were most stable during the period the futures market was open, even considering that market manipulation was rampant. The study is sixty years old now, and onion farming has, I assume, changed plenty since, but the finding has never really been debated, at least on the niche Onion Futures advocacy side of Twitter I live on. Nevertheless, he was directionally correct 60 years ago and is still correct today. Onion futures made onion prices more stable.

The 2008 commodity boom put this to a point once again, this time in a more public, less academic space. While Congress hauled in witnesses to ask whether speculators were driving up oil, Fortune’s Jon Birger noticed that an entirely separate, neglected asset was behaving with far greater instability, a crop that Capitol Hill had effectively abandoned to the winds. Onions had been more volatile by orders of magnitude, compared to all of the futures-based commodities that Congress was mad about: onion prices rose about 400% from late 2006 to spring 2007, crashed, and rebounded, while oil, the supposed “casino” of the commodity industry, was as flat as a table by comparison.

Bob Debruyn, whose father was among the Michigan growers who originally lobbied for the ban, told Fortune that “there probably has been more volatility since the ban” and that a futures market for onions would make sense today. When the farming family that asked for the law starts wondering aloud, the law is polling badly.

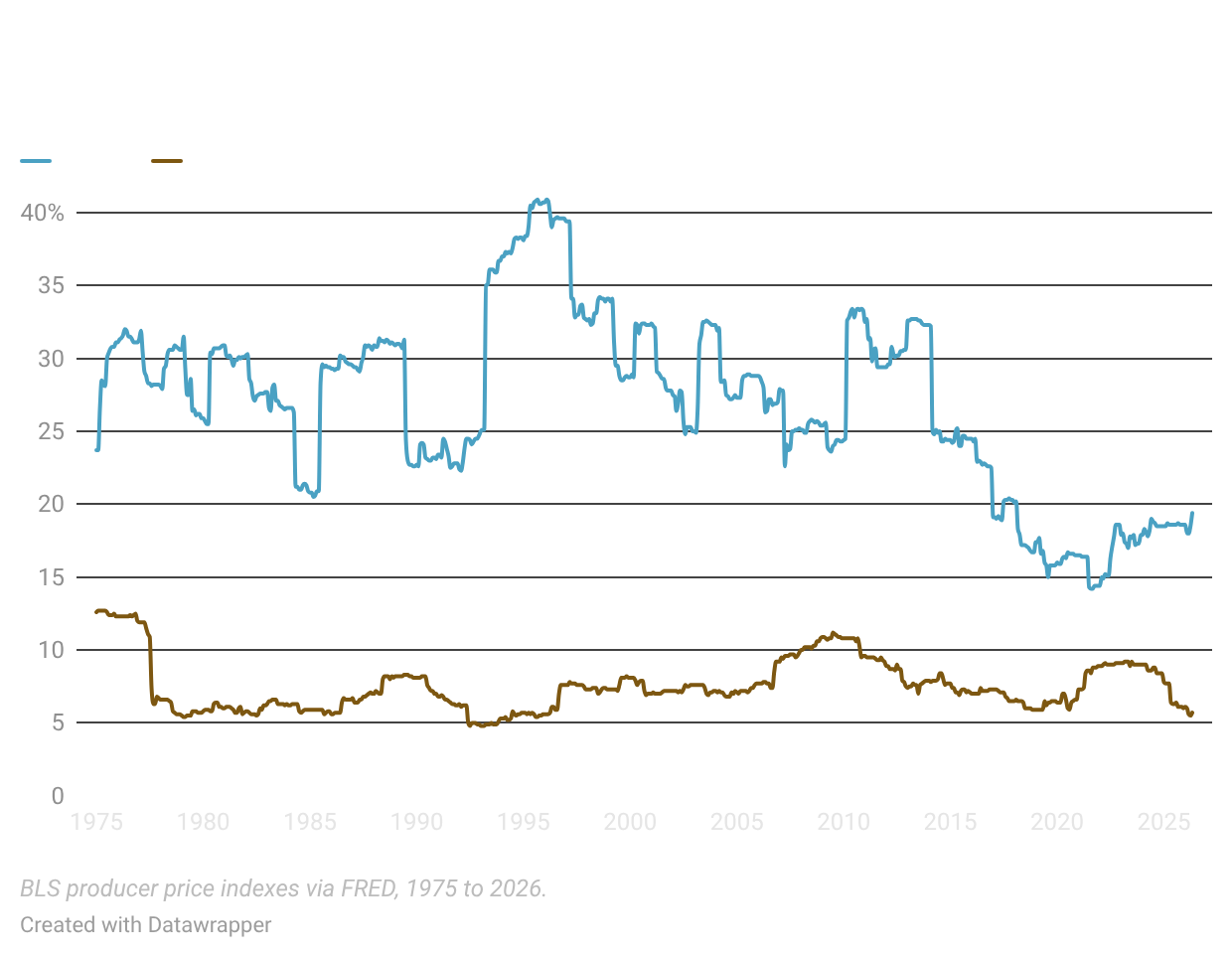

And if a story about 2007 feels like cherry-picking, a very valid critique, stretch the exposure out. Measure the volatility of monthly price moves on a rolling four-year window, so no single year can dominate, and run it from, let’s say, the 1970s up to today, checking both onion and corn prices. The gap between the two is not an episode. It is a property of what onion trading has become.

The fair objection is that onions were always a hard market to trade, as many food and produce-based commodities are. They rot; they cannot sit in a silo for two years the way corn can, and to top it off, the market is not a hegemon of our financial system; the whole US onion crop is small enough that a determined pair of traders once bought most2 of it, which is how we got here.

Maybe a revived onion contract would be thin, and maybe it would fail for the reason most contracts fail, which is that nobody needs it. But, I really believe, there is a difference between letting a market die of natural causes, rot per se, and artificially killing it. Futures now trade on plenty of things more perishable than an onion, milk and lean hogs among them, and cash settlement has long since solved the problem of nobody wanting a boxcar of sprouting Vidalias, on a contract they forgot that they held until delivery.

The 1958 objection is a 1958 objection.

However, not all hope is lost. Recently, fellow onion stability enthusiasts from the University of Chicago launched a campaign called “For Our Futures.”, Lately, their efforts have been largely confined to campuses like the University of Chicago and Northwestern. However, I am convinced that cultivating awareness among the American student body is a vital lever for elevating this neglected, yet deeply significant, legislative oversight to the national stage.

The single commodity future that has ever been banned from speculation has spent seven decades as the most unstable item in the produce aisle, more volatile than oil, out-swinging corn, and the stability the ban promised shows up nowhere in the data, not in 1963 when Gray went looking and not in the fifty years of price history aforesaid. Repealing it would cost next to nothing, give onion growers the same insurance every corn farmer takes as God-given, and would close the books on the strangest law in American financial history. It is a rare legislative opportunity: a bill that fixes a broken market and, quite literally, makes it less likely for anyone to cry.

This is actually true. It is often faster and easier to buy extremely out-of-the-money call options versus just burning it with gasoline if you’re dealing with large amounts of money.

Today’s market has swollen considerably, and a number of modern safeguards would render cornering the market not just technically infeasible, but bordering on the absurd. Still, the fundamental reality remains: it is a marketplace effectively dwarfed by the massive, liquid giants like corn and crude oil.

| A guest post by

|

Nice article Ryan!