The Right to Ask a Question

Mustafa Aljatery, Polymarket’s senior intern, posted this week that all Polymarket users are now permitted to sponsor rewards pools for markets.

He says, “permissionless market deployment and creator fees next…”

Bayesian Supercycle is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

When I read this, I immediately thought of Scott Alexander’s recent post about this, what he called the “original Manifold vision.”

A prediction market site which offers:

Real money markets

…that are user-created, user-resolved, and potentially subjective, giving the user a percent of the volume as a reward for writing/managing/promoting the question.

…and are otherwise easy to use (good interface, high volume, legal in the US)

…

When I ask Polymarket why they won’t do 2, the answer is a combination of regulatory issues, fear that people would write bad resolution criteria and it would reflect badly on them, and there always being something more important to do. I haven’t asked Kalshi, but their answer would definitely be regulatory.

But this recent tweet gives reason to think that’s the direction they might be shifting in, and Chairman Selig’s remarks from yesterday morning show a softening in regulation.

This isn’t all hype; we are beginning to see actual changes in how the CFTC regulates DCMs (Designated Contract Markets). In January, Xchange Alpha was designated as a DCM just 204 days after their application, the fastest designation in CFTC history.

A contributing factor to this recent policy shift was propagated by PM-related ventures from the Trump family. Don Jr. is a senior advisor to both Polymarket and Kalshi, and Truth Social, Trump’s social media network, is set to launch Truth Predict, a prediction markets platform. (Prop bets here.)

In short, there’s a lot of regulatory wiggle room for not only new players, but shenanigans from established exchanges. It’s possible Polymarket could have a route to adding user-created markets.

Regulation and Responsibility

The primary regulatory issue with a user-created market program is that DCMs are partially responsible for all the listed event contracts that are tradable on their exchange. This means that they are responsible for enforcing the policies outlined in their rulebook,1 which usually includes exclusively listing contracts that are not susceptible to manipulation2 and maintaining clear-cut resolution criteria.

Part 40 of Title 17 Regulation (the code that governs the CFTC and SEC) explains how a DCM is permitted to list a new contract. They can self-certify, where the exchange has to file online, certify that the listing complies with the Commodities Exchange Act, and wait one business day before listing. Alternatively, they could request full approval directly from the CFTC, which requires a waiting period of 45+ days (not practical for a user-created market program). The CFTC also reserves the right to remove any contracts they believe are “contrary to the public interest.”

This means Polymarket would have to individually approve each submitted contract, which goes against the original “permissionless market creation” proposal. It seems like this system would essentially be a formalized way of market suggestions.

Core Principles of an Exchange

Part 38 of Title 17 Regulation details the twenty-three Core Principles required by an exchange to be designated as a DCM. The exchange must comply with these at all times, or else they run the risk of their designation being revoked. Below are some Core Principles that may impact Polymarket’s ability to offer a user-created markets program.

Core Principle 3: Listing Markets that are not Susceptible to Manipulation

This is probably the most important Principle to consider. Appendix C to Part 38 details which markets are susceptible to manipulation:

Cash settled contracts may be susceptible to manipulation or price distortion. In evaluating the susceptibility of a cash-settled contract to manipulation, a designated contract market should consider the size and liquidity of the cash market… situations susceptible to manipulation include those in which the volume of cash market transactions and/or the number of participants contacted in determining the cash-settlement price are very low. (c)(2)

This limitation essentially says that all markets must have a reasonable amount of liquidity, so user-created markets with low amounts of liquidity wouldn’t be very feasible…

Where an independent, private-sector third party calculates the cash settlement price series, the DCM should verify that the third party utilizes business practices that minimize the opportunity or incentive to manipulate the cash-settlement price series. (c)(3)(i)

This means that there would have to be a system in place to prevent any incentive for a market creator to misresolve a market. There are certainly workarounds for this. For example, Polymarket could set up automated resolutions using APIs (for quantifiable measurements like stock prices, weather, etc.) or AI for more current news-related markets.3

Where the contract is settled to a third party cash-settlement series, the DCM should consider the nature and sources of the data comprising the cash-settlement calculation. (f)(2)

This means that Polymarket would have to be constantly checking and verifying the resolution data is coming from accurate sources.

Core Principle 4: Prevention of Market Disruption

Polymarket would need to maintain authority and close watch over the markets to prevent exploits and manipulation. This bottleneck exists with their current markets, but scaling that to accommodate tens of thousands of user-created markets would be exceedingly difficult.

A DCM must…

(a) Collect and evaluate data on individual traders' market activity on an ongoing basis in order to detect and prevent manipulation, price distortions and, where possible, disruptions of the physical-delivery or cash-settlement process…

(c) Demonstrate an effective program for conducting real-time monitoring of market conditions, price movements and volumes, in order to detect abnormalities and, when necessary, make a good-faith effort to resolve conditions that are, or threaten to be, disruptive to the market (38.251)

This is already done primarily through automation, but it would have to be scaled to a much larger level in order to monitor the influx of trading that would come with user-created markets.

Potential Workarounds

I see two options forward, probably in a similar way that Polymarket once saw their options before they became an exchange for event contracts.

1. Offshore Wild West

Create the platform on the non-US exchange and instate little oversight or moderation, and see what happens because, after all, the CFTC can’t do anything about the global exchange. At first glance, this seems like (a) a very Polymarket sort of thing to do (b) a way for Polymarket to lose a huge amount of credibility and (c) an absolutely horrible idea.

2. The Complicated Regulatory Route

Here’s a couple ways Polymarket could approach this.

The Rulebook Amendment Path

Polymarket submits an amendment to their rulebook, spends a huge amount of money to lobby the CFTC, and gets rubber-stamped by the Commission.

A Complex System that Meets Regulatory Requirements

There could be a system where users can submit market suggestions and traders can vote on which ones to accept, ensuring each market would have a sufficient amount of traders and liquidity, and Polymarket could make a large investment into advancing their trading monitoring algorithms. They’d also avoid trading fees to avoid regulatory issues related to Introducing Brokers and other complex rules surrounding that, in addition to not accepting suggestions that don’t have clear-cut public resolution criteria.

Would this even be good for society?

Setting aside the regulatory challenges involved, it’s not certain whether this would even be a “good” development for the PM industry. Here’s what I see:

The Good

Experimental Markets for Research

This would allow anyone to be able to make markets that could be useful for academic research or otherwise provides valuable information about market mechanics. For example, here’s a LLM-focused market I made on Manifold over the summer:

Or futarchy experiments:

Robin Hanson has also run experiments in which prediction markets were used to determine which scientific research projects would have the most effect, which also seem to be a high-value usage of PMs.

These sorts of markets are my favorite part of Manifold, and it would be great if these sorts of mechanisms could become part of the public view into the PM industry.

Eliminating Biases in Market Creation

Many Polymarkets seem to be niche or insignificant compared to other topics they could be featuring. For example, trading volume about crypto prices on PMs far outweighs those on stock prices, even though stocks have a much higher trading volume in their non-derivative forms. Think about something like mention markets, they’re very random and high-volume whereas more impactful markets like the ones I described above don’t even exist.

Leveling the Playing Field

PMs are heavily intertwined with crypto in a way that makes newcomers who are unfamiliar with crypto challenging to enter the market landscape. Crypto bros care about very specific topics that may not appeal to the general public, so user-created markets would hopefully open up the range of topics available to trade on.

Insurance and Hedging

A persistent use case of PMs has been hedging against risk. User-created markets could expand this to every type of insurance that you would possibly need. Of course, markets hedging against physical risk have the dangerous possibility of manipulation of the outcome, but otherwise it is useful because other traders would most likely provide better odds than insurance companies.

Reliability

Recently, many specialized exchanges have been focusing on specific types of markets, such as hedging AI compute (1, 2). These exchanges remain illiquid and are often unreliable to trade on, especially those that are not DCMs. It’s better to concentrate many markets in the largest exchanges to avoid forcing traders that need to hedge something to go to small, illiquid exchanges.

The Bad

Manipulation

The reason the CFTC regulations exist is to prevent theft, fraud, and manipulative behavior. When Polymarket is not forced to respect these guidelines, all accountability is absolved and the exchange can make whatever decisions he wants to. As you could imagine, this is dangerous.

Spam Markets

Rather than useful markets, most markets will probably fall in the opposite category, focusing on insignificant mentions and other ambiguous events such as those that are frequently cluttering the Manifold home feed. User-created markets would basically be the “shitcoins” of Polymarket.

Signal Reduction

Having many illiquid markets may be distort the signal quality of the market, defeating the purpose of making a PM in the first place.

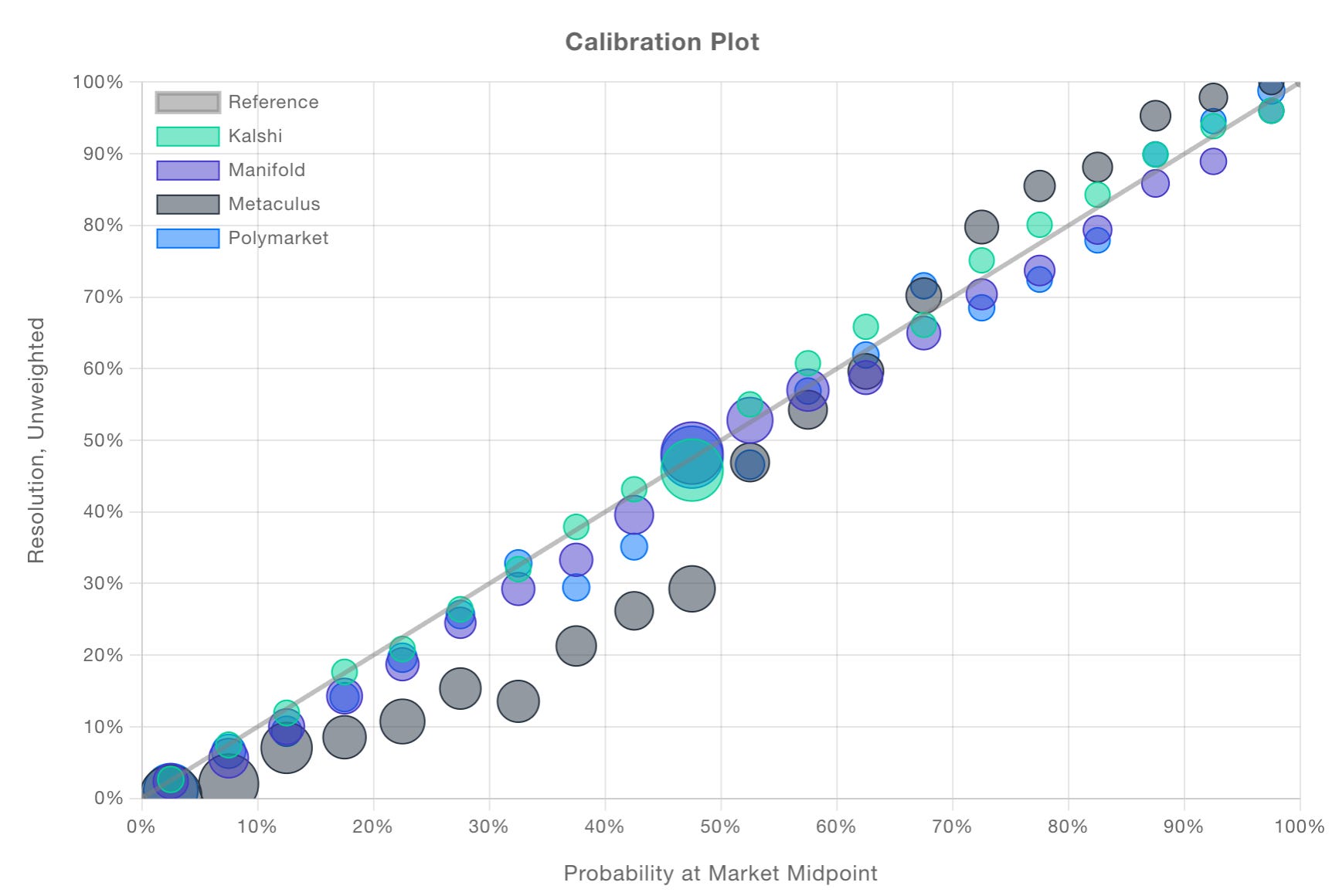

On the other hand, Manifold is nearly as accurate as all of the real-money exchanges, so this may not be a concern.

Regulatory Trailblazing

If Polymarket were to implement this on a global or US scale, it would have a massive influence on future small exchanges and make the regulation even softer. This would lead to all of the bad parts about these markets being amplified.

How realistic is this?

On the global scale, this decision is more about product and brand identity than actual regulatory barriers. I could definitely see something like this rolling out on the global front, but I’m not sure about the end of 2026 time horizon. I think there’s a huge amount of pushback against the recent PM boom and it would be a dicey PR decision for Polymarket to introduce these now. When PMs further integrate into society and become common technology, I see user-created markets as more of a given than a feature. I would assign the roll-out of user-created markets about a 15% probability by the end of the year, and about 25% by the end of 2027.

On the US scale, I would give this a <5% probability of rolling out by the end of the year. Even though the CFTC has been aggressive in its stance to attack states who challenge PMs and protect the exchanges, the regulation can only get pulled back so fast. I could see Trump family ventures such as World Liberty Financial and Truth Predict playing a major role in the regulatory decisions. If Trump wants to have user-created markets, he’ll certainly be able to make that happen. But Truth Predict is still in its early stages and I see this coming later. Polymarket also continues to be on shaky ground from a regulatory standpoint, having only been designated in January and previously being illegal in the US.

If user-created markets launch on any major exchange, it would be a structural shift for the entire industry. I hope that exchanges will recognize how they can best advance PMs to be used for the public good, and I’m looking forward to seeing what comes next.

Disclaimer: I used AI to assist with legal research and comprehension, but the text and outline were entirely human-written.